The Southeast Energy Exchange Market, or SEEM, may look like an energy imbalance market from the outside, but a look under the hood reveals a different story.

A Great Plains History Lesson

Energy imbalance markets have been precursors to the transition to a Regional Transmission Organization. In the Southwest Power Pool, the Energy Imbalance System introduced hourly prices for the differences between schedules and actual requirements for individual generators using a Locational Imbalance Price. The LIP, as it was called, was basically a Locational Marginal Price but was only applied to imbalance energy, and not the entire delivered or consumed power requirement. Within a few years, SPP built upon the EIS platform and evolved into a full-blown energy market.

The Western Transition

More recently, the Western Interconnection has seen the spread of the CAISO Energy Imbalance Market into Arizona, Nevada, Utah, Idaho, Washington and Oregon, with expansion into Montana, Colorado and New Mexico over the next two years. The EIM structure is similar to the SPP Energy Imbalance System with the use of locational prices for calculating a real time price for schedule deviations.

The Southwest Power Pool has taken lessons learned from their EIM development and is preparing to roll out a Western EIS, but that effort has slowed down due to regulatory concerns regarding their tariff. The WEIS still maintains a structure that relies on an intra-hour LMP price signal for any generator or load located within a participating Balancing Authority.

A Southeast Perspective

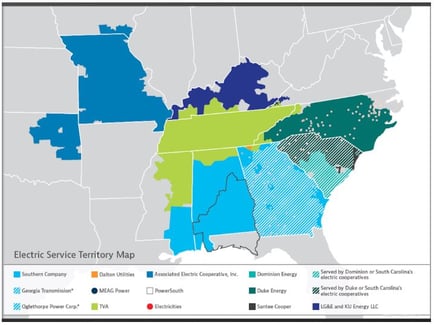

Map of utilities involved in SEEM discussions, courtesy of Charlotte Business Journal

Whether or not it has been intentional, Southeast utilities have been unsuccessful in achieving any sort of regional transmission organization or independent system operator. Initiatives like GridSouth and SETrans did not get off the ground for various reasons.

It appears that Southern Company and Duke Energy are now spearheading the SEEM effort with input from other regional utility stakeholders. Unlike the aforementioned Western EIM and SPP EIS, initial reports regarding SEEM indicate that this initiative does not appear to possess many of the qualities that result in significant savings with real-time balancing markets such as transparency, liquidity and competition.

Things to Consider

- Pricing: Under SEEM, it appears utilities will communicate their bids to either sell excess generation or to purchase to cover deficiencies. The cost of power does not have to be based in reality, but only what the “market” will bear. This type of automated, bid-based “split the savings” system was a hallmark of the Florida grid going back to the 1980’s and proved to be an effective way to transact prior to FERC Order 888. A Locational Price structure, such as what is used it RTOS throughout the continental US, is designed to put downward pressure on prices which results in greater savings to consumers.

- Deliverability: With an automated, bid-based system between Balancing Authorities, SEEM transactions would likely require real-time assessments of infra-hour Available Transfer Capability and approval of eTags. With both the CAISO and SPP EIMs, transmission is non-firm, “as available” and is priced at zero cost. The cost and curtailment priority of SEEM transmission versus other non firm products is something that will need clarity.

- Participation: There are still questions to be answered with respect to who gets to be part of SEEM. LMP-based systems allow for all generators to have their imbalances settled with a real-time price signal. If third parties are not allowed to bid or if third parties have to procure an intra-hour transmission product on a 15-minute, then the only way they could take advantage of SEEM is to be a designated network resource of a participating utility.

The GDS View

There is still much more to be done before a full assessment of SEEM can be performed. We expect that further discussions with state utility commissions must occur, particularly in the Carolinas where the state legislators are already pushing for regional transmission organizations and real-time energy markets. It is anticipated that economic studies to assess benefits are forthcoming soon which means that there will be winners and there will be losers. Eventually, market rules and tariffs will need to be filed with FERC, which will require detailed evaluation of the impacts on those who did not have a seat at the table. The regulatory pressure to move the Southeast toward an RTO will likely grow as more renewable generation penetrates the region. Our recommendation is to identify your strategic goals, find any allies and be ready to move quickly.

For more information or to comment on this article, please contact:

For more information or to comment on this article, please contact:

John Chiles, Principal-Transmission Services | CONTACT

GDS Associates, Inc. – Marietta, GA

770-799-2423 or john.chiles@gdsassociates.com