INTRODUCTION:

The past few years has seen a surge in reactive power compensation filings for solar and wind-powered projects, with a high concentration of filings for facilities in MISO and PJM. There are several factors contributing to this trend. Spurred on by decreasing costs, state and regional renewable energy goals, and investment tax credits (ITC), solar leads all other technologies for new electric generation capacity additions. Together solar and wind outstripped all other technologies 4:1 in new U.S. capacity additions in 2020. Until recently, reactive power compensation for wind and solar was not an achievable revenue opportunity, but technological advancements and changes in the regulatory landscape created new revenue opportunities for non-synchronous resources. And since PJM and MISO are the most lucrative markets for reactive compensation, it is not surprising to see the number of solar and wind projects seeking reactive compensation at the Federal Energy Regulatory Commission (“FERC” or the “Commission”).

HISTORIC PERSPECTIVE: REACTIVE POWER REQUIREMENTS FOR SYNCHRONOUS AND NON-SYNCHRONOUS GENERATION

Order No. 2003 - In Order No. 2003 Standardization of Generator Interconnection Agreements and Procedures, the Commission adopted standard procedures and a standard agreement for the interconnection of Large Generating Facilities, which included the reactive power requirement. Under this requirement, facilities must be designed to provide 0.95 leading to 0.95 lagging reactive power at the Point of Interconnection. Subsequently in Order No. 2003-A the Commission recognized the pro forma interconnection agreement was designed around large synchronous generators, and determined that generators relying on newer technologies with unique electrical characteristics (i.e., wind generators) would be exempted from this reactive power requirement.

Order No. 827 -The next significant Commission order for non-synchronous generators’ requirements for reactive power came with Order No. 827, Reactive Power Requirements for Non-Synchronous Generation. In this order, the pro forma LGIA and the pro forma Small Generator Interconnection Agreement (“SGIA”) were revised to require new non-synchronous generators to provide dynamic reactive power, recognizing that the equipment needed to provide reactive power had become more commercially available and less costly.

However, acknowledging the differences in technologies between synchronous and non-synchronous generators, Order No. 827 altered the point of measurement of reactive capability for non-synchronous generators from the Point of Interconnection to the high-side of the generator substation.

COMPENSATION FOR REACTIVE POWER

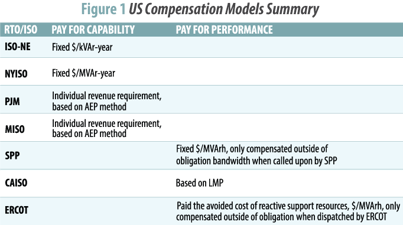

Generally, compensation can be categorized as either “pay

for capability” or “pay for performance.” Figure 1 presents a summary of the compensation models throughout the United States. Although ISO-NE, NYISO, PJM and MISO all pay for capability, compensation in PJM and MISO are most lucrative since the compensation is an individual cost-based revenue requirement, based on the AEP Methodology. That is the higher the costs to provide the service, the higher the compensation. Additionally, several markets also compensate generators providing reactive service for variable costs, such as lost opportunity costs, cost of energy consumed, and/or cost of energy produced, when called upon to produce MVArs instead of MW.

Figure 1 presents a summary of the compensation models throughout the United States. Although ISO-NE, NYISO, PJM and MISO all pay for capability, compensation in PJM and MISO are most lucrative since the compensation is an individual cost-based revenue requirement, based on the AEP Methodology. That is the higher the costs to provide the service, the higher the compensation. Additionally, several markets also compensate generators providing reactive service for variable costs, such as lost opportunity costs, cost of energy consumed, and/or cost of energy produced, when called upon to produce MVArs instead of MW.

AEP METHODOLOGY AND ADAPTATION FOR NON-SYNCHRONOUS GENERATORS

While the Commission has not required a uniform approach

to compensation for reactive power, the FERC-approved AEP Methodology is the precedent for calculating cost-of-service reactive service compensation in a “pay for capability” compensation model, such as in MISO and PJM. This oft-cited method originated with AEP’s 1993 FERC rate case to determine an annual revenue requirement for its fleet of thermal (coal) generators.

The method depends in large part upon the FERC Uniform System of Accounts (“USofA”) to allocate investment in specific components supporting production of reactive power based on the accounting treatment for that plant, and applies an annual fixed charge rate to that investment to arrive at the annual reactive power revenue requirement.

The AEP Methodology has since been adapted for non-synchronous resources. In doing so, applicants liken the function of key components addressed in AEP to the specific components characteristic of non-synchronous generators, such as solar panels, AC and DC collection systems, wind turbines, and inverters.

However, the adaptation of AEP for non-synchronous generation is not without criticism or controversy. Common objections to the interpretation of AEP to non-synchronous generation include:

- Proper accounting for wind and solar plant costs,

which is now the subject of a rulemaking before the

Commission; - Attribution of non-synchronous components by

function to that of typical synchronous generator

components supporting reactive production; - Allocation of components to Accessory Electric

Equipment supporting production of reactive power,

i.e., the “AEE Allocation Factor;” and - Demonstrated reactive capability vis-a-vis use of

nameplate Power Factor (“PF”) of the invertors in

calculating the Reactive Power Allocation Factor.

REACTIVE REVENUES PAID TO SOLAR AND WIND GENERATORS

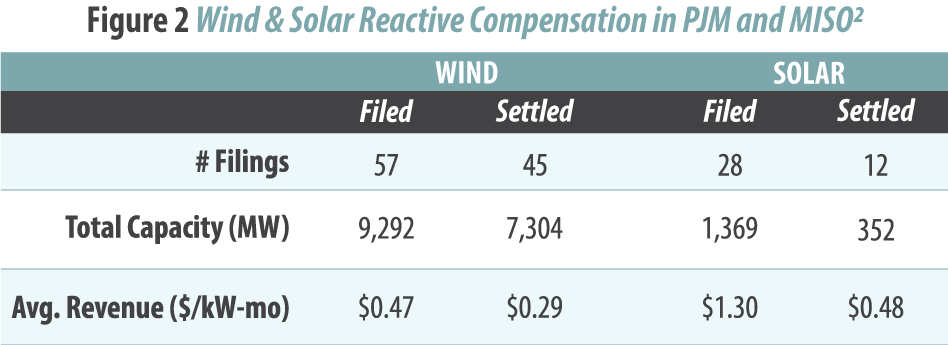

Current practice at FERC is, with limited exceptions, to set all reactive filings for hearing and settlement proceedings. Most reactive filings are settled without going to litigation at some reduction to the filed rates. For wind and solar filings, the settlement process typically results in a significant reduction to the as-filed annual revenue requirement (“ARR”) (see Figure 2).

Two key objections to continue using AEP as precedent for

Two key objections to continue using AEP as precedent for

determining revenues for non-synchronous generations are that (1) the reasonableness of paying reactive compensation based on a method that does not account for the intermittency of non-synchronous generation (no wind, no sun, no power);

and (2) the as-filed ARRs for non-synchronous resources resulting from the modified AEP approach are notably higher than that of comparably sized synchronous generation. Despite the reductions taken in settlement, MISO and PJM solar and wind revenues are nevertheless on average two to five times greater than those paid to steam, combustion turbine or combine cycle generators on a $/MW basis, based on Q4 2020 data for reactive revenues paid in MISO and PJM.

RECENT EVENTS DRIVING CHANGE

Spurred by the exponential rise in renewable generation,

particularly from the independent power production sector over the past several years, stakeholders in both MISO and PJM are investigating alternative rate designs for reactive power.

A common element to both the MISO and PJM rate designs is there is no cap on the amount of reactive capability for which the ISO/RTO will compensate. That is, regardless of need for additional reactive service, if a generator’s compensation request is approved by the Commission and it meets the ISO/RTO technical requirements then the applicant recovers the

approved revenue requirement.

As previously discussed, the adaptation of the AEP method

used by several expert witnesses in this field yields as-filed ARRs significantly higher on a dollar-per-MW basis compared to synchronous generation. Protesting parties routinely identify the general inapplicability of AEP and specifically the criticisms described previously as key issues in the filing.

In an attempt to resolve some of these issues, on April 28, 2020, Locke Lord LLP filed a request for confirmation from the Chief Accountant at the FERC that the cost of specific wind and solar generating equipment is properly booked to FERC Account Nos. 343 - Prime Movers. 344 - Generators, and 345 - Accessory Electric Equipment, in Docket No. AC20-103-000.

On January 19, 2021, the Commission rejected Locke Lord LLP’s request, but concurrently opened a Notice of Inquiry (NOI) on

the accounting and reporting treatment of certain renewable

energy assets under Docket No. RM21-11-000. The NOI solicited

comments on (1) whether the Commission should create new

accounts for non-hydro renewable generating assets in the USofA, (2) revisions to FERC Form No. 1 to reflect any such new accounts, (3) whether the Commission should codify the proper accounting treatment of renewable energy credits, and (4) the rate implications of these potential accounting and reporting changes (i.e., impact on reactive power rates).

EVOLVING LANDSCAPE AND CONSIDERATIONS

Owners of renewable generation will continue to optimize

revenue streams and to seek those revenues in the most lucrative markets. There is growing momentum in both MISO and PJM to address the current reactive power compensation construct, and that, coupled with activity at the Commission with the NOI, other non-ISOs/RTOs will likely follow suit and/or look to the outcome of RM21-11 to decide the best model for their ratepayers. That said, no formal proceedings have begun to initiate a change to Schedule 2 in MISO or PJM.

The Commission may propose changes to the USofA that

include new account categories to address new technology and the accounting treatment thereof, but it is likely that this will take more than three years to finalize.

As an electric utility, it makes sense to consider the repercussions of all reactive rate filings within the transmission zone which may require intervening in reactive revenue dockets to express specific concerns. It’s also helpful for electric utilities to identify opportunities to optimize potential reactive revenues from the utility’s generation resources to lower transmission cost for retail customers.

For more information or to comment on this article, please contact:

Michele Slater, Senior Project Manager | CONTACT

GDS Associates, Inc. – Marietta, GA

407-563-4463 or michele.slater@gdsassociates.com