For the past several years and notwithstanding the economic woes, growth in residential household load usage has been subdued by the impact of increased efficiencies in electric appliances. Government regulations in the past have called for more efficient HVAC systems, light bulbs, windows, insulation in new construction, etc. and the electrical industry is starting to see the impact on residential load forecasts. Utilities are coping with the fact that average use just isn’t growing the way it was in the latter part of the 20th century. There was a time when not everybody had a refrigerator, or a washer and dryer, or multiple TV sets. But now it’s the norm. These appliances are more affordable today than they were 50 years ago. Most people now have these appliances, and these markets are quickly becoming saturated. Saturated markets, increased efficiencies, and competitively low natural gas prices are the biggest reasons why average use projections are relatively flat for several years with longer-term growth coming from miscellaneous plug loads (iPads, laptops, cell phones, etc.). Utilities would love a new “washer and dryer” load to boost average use and ultimately revenue.

Imagine a typical residential consumer has just purchased a new PEV. They arrive home at 5:30 from a long day of work, go inside and start cooking dinner, catch the news, and bump up the AC. Then, from a utility standpoint, something scary happens. The customer nearly double the house’s load by plugging in the PEV and allowing it to charge overnight. They are not thinking about the system ramifications and they do not care about the additional stress that is being put on the transmission and distribution lines that bring power to their home. The problem becomes even more magnified when potentially hundreds of their peers are doing the same thing across the system and adding demand during on-peak hours. So what can a utility do to reap the benefits of additional sales without purchasing new capacity?

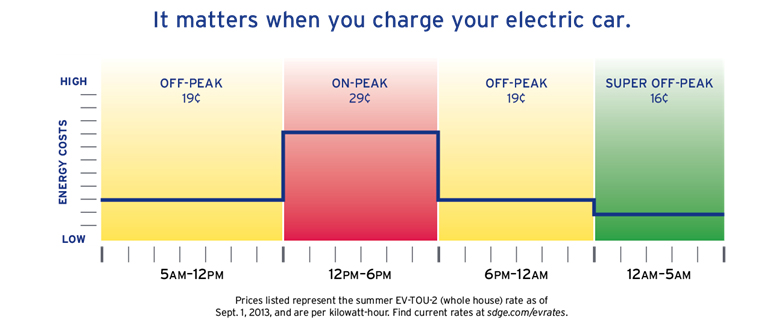

AMI: AMI meters provide utilities incredible amounts of data regarding residential usage characteristics. They have enabled utilities to monitor system peaks instantaneously. In the past, they have been used to develop Time-of-Use rates for a user as a whole. Now, they’re being used to develop Time-of-Use rates for independently metered charging stations. With knowledge of the average PEV load shape, utilities are able to send price signals to customers that will incent them to charge their cars overnight as opposed to during peak times. This is a great way that a utility can take that PEV load and use it to improve system load factors and increase revenue while not adding any peaking load to the system. Below is the rate structure for San Diego Gas and Electric’s EV TOU 2 rate.

The price signal doesn’t get much clearer than this with users paying as much as a $0.13 per kWh premium to charge during peak times. AMI meters give utilities the ability to implement dynamic pricing programs for residential consumers.

Demand Response: Utilities have been enacting demand response (DR) programs for decades. The concept is not new. Utilities hope to, in the near future, use a similar technology to turn off charging stations and force users to charge during off-peak periods. This will enable utilities to shape the load of PEV charging.

V2G: Perhaps the more visionary PEV smart grid technology is called Vehicle-to-Grid (V2G). While the practice is not yet widespread, researchers at the University of Delaware1 are on the forefront in developing a method for pulling energy from PEV battery packs, and distributing to the grid. It turns out that, if and when PEV market share increases, utilities may find the home as a source for capacity. It will be interesting to see how this research unfolds and impacts the industry.

As electric vehicles gain in popularity, utilities will need to begin to consider the important implications outlined above, including ways to manage the residential load shape. Another important question, from a planning perspective, is just how much PEV related load should be included in load forecasts?

President Obama declared in his 2011 State of the Union Address that, “With more research and incentives, we can break our dependence on oil with biofuels, and become the first country to have a million electric vehicles on the road by 2015.” This was a bold claim for a nation that, just the year prior, purchased more than 60% more Ford F-150’s than the leading mid-sized sedan, Toyota Camry. Specifically, President Obama stated that the Chevrolet Volt would make up roughly half of the 1 million electric vehicles on the road by 2015. By the end of 2013, less than 55,000 Chevy Volts had been sold, a far cry from the projected 250,000 the President had expected at this point. By the end of 2013, Americans had purchased just shy of 100,000 PEVs, out of a total of over 15.6 million light vehicle purchases. Obviously, PEVs are not taking the US by storm yet. Part of that can be blamed on the $40,000 sticker price of a Chevy Volt and part of that can be blamed on the lack of PEV alternatives. Through 2011, there were really only two PEVs to choose from. Along with the Chevy Volt, there was the Nissan Leaf.

Load forecasts are not likely to see a measurable impact from PEV in the next several years. It does, however, depend on the location of your utility. Currently, large west-coast cities such as San Francisco and Los Angeles hold the highest percentage of PEV on the road, accounting for 19.5% and 15.4% respectively. This is largely due to the charging station infrastructure that these cities have already built. Consumers are less likely to buy a PEV if they can only charge it at home. Furthermore, it is likely that adoption will move from urban to rural areas as a natural progression in how the infrastructure will be built. Therefore, municipal utilities and IOUs, especially in progressive regions of the country, will likely deal with noticeable and measurable PEV loads before rural cooperatives. As demand for PEVs grows, so too will the infrastructure to smaller cities and eventually rural areas. It’s the perfect time to start thinking about PEV integration.

References

1. https://www.udel.edu/V2G/

For more information or to comment on this article, please contact:

Andrew Henson, Analyst | CONTACT

GDS Associates, Inc. – Marietta, GA

770.799.2403

DOWNLOAD PDF

Also in this issue: Agriculture Energy Management Plans Benefit Farmers and Electric Utilities

{kind=link}